The Hydrogen Revolution and What it Means for Switzerland

Kateryna Holzer*

1. Swiss Green Transition

In the aftermath of the Fukushima nuclear catastrophe in 2011, the Swiss government adopted the Energy Strategy 2050, a central element of which was a progressive withdrawal from nuclear energy production till 2032 and an increase in energy efficiency and generation of renewable energy. For the latter, Switzerland relies heavily on its abundant hydropower resources making efforts to further expand it to the level it used to have in the 1970s when hydropower accounted for almost 90% of domestic electricity production. However, in recent years attention has increasingly been paid to the potential of hydrogen in supporting the goals of the Energy Strategy and net-zero economy. With the ample hydropower making the price of electricity comparatively low, Switzerland has great potential to become the world’s leading country in hydrogen production. For Switzerland, hydrogen is especially interesting for seasonal energy storage to store solar energy produced in large quantities during summer months. The hydrogen storage with a seasonal cycle is a necessary complement to the battery storage with a daily cycle.

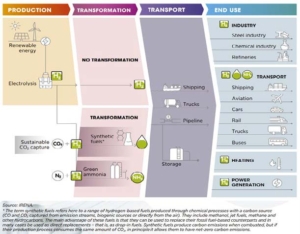

2. H2 as the Magic Formula for a Net-Zero Economy

According to some estimates, the use of hydrogen produced from electrolysis using electricity from renewable energy may account for 20% of all emissions reductions necessary for the achievement of the net-zero goal by 2050. In the IRENA 1.5°C Scenario, hydrogen would meet 12% of the final energy demand. Like electricity, hydrogen is not a primary energy source but an energy carrier, which is especially valuable for energy storage for renewable energy and also for the hard-abating sectors of the economy, such as the transport and steel sectors. Hydrogen has huge potential not only in decarbonization but it can also drive economic growth (see figure below).

Hydrogen can be of various carbon footprints designated by different colors. The majority of hydrogen produced today is grey (over 85% of all hydrogen), which is resulted from steam methane reforming. This production process can result in blue hydrogen, however, if CO2 is captured by carbon capture and storage methods (from 68% to 98% of CO2 can be captured). However, what is needed for a net-zero future is green hydrogen, which can be produced by means of electrolysis of water with the help of electricity from renewables. Various national and regional certification schemes are used to distinguish among different types of hydrogen produced. They are based on various standards and definitions of green or clean hydrogen and there is no unified methodology. What is particularly important is the development of unified standards related to the safety issues of hydrogen in storage and transportation because of the high risk of flammability and explosion when hydrogen comes in contact with air.

3. The Role of Regulatory Incentives in the Development of the Hydrogen Economy

Currently, the share of green hydrogen is only around 4% of all hydrogen produced in the world. The production of green hydrogen is very costly, primarily because of the high costs of electrolysis, as well as storage and transportation of hydrogen (this requires either transforming it in liquid, compression, or storage in ammonia). The latter requires building the necessary infrastructure, including pipelines, compression units and hydrogen refueling stations, and fuel cells. Therefore, at this stage, it is urgently needed to create incentives for investments in green hydrogen production and develop a fully-fledged market, bringing producers and consumers together. More stringent emissions restrictions and subsidies in the form of tax exemptions provided to producers who use hydrogen technologies are very important in this respect. Experts believe that the future drop in prices above all depends on carbon price policies based on emissions trading or carbon taxes. Cooperative approaches under Article 6 of the Paris Agreement can also be very useful in this respect, as they can direct financial resources from developed countries to developing countries with abundant renewable energy resources (e.g. solar) for more efficient production of green hydrogen.

Many countries have started developing policies and measures in support of the hydrogen economy. For instance, in the US, under the recently adopted Inflation Reduction Act (IRA), the incentives for the expansion of green hydrogen include the provision of production tax credits for 10 years, investment tax credits for energy storage, clean vehicle credits to vehicles that use hydrogen fuel cells (as well as electric batteries) and also alternative fuel credits in the form of property tax credits for hydrogen fueling stations. As a result, the installed hydrogen capacity in the US is expected to increase from the current 2 GW to 12 GW by the end of the decade. In general, due to supportive policies across the world, it is projected that Europe will drive the growth of installed hydrogen capacity with 50 GW added to cumulative capacity by 2030, followed by Australia with 34 GW, Africa with 25 GW, and Latin America with 17 GW. Economic incentives are really important. According to a study, a $3 tax credit for every two kilograms of hydrogen produced is able to bring down the cost of green hydrogen to that of grey hydrogen.

4. Hydrogen in Switzerland

Unlike the EU and nearly 30 other countries, Switzerland has not yet adopted a hydrogen promotion strategy. The domestic production and trade volumes of hydrogen in Switzerland remain very small, primarily associated with a number of pilot projects recently launched. One of the most significant of them is XCIENT, a Swiss-Korean Hyundai fuel cell truck project. By 2025 it would supply a total of 1,600 hydrogen fuel cell heavy-duty trucks to Swiss supermarkets and other logistics companies that can receive these trucks in lease. This project is run by a joint venture established with the Swiss hydrogen energy company H2 Energy. In support of the project, the Swiss government exempted companies using the trucks from the heavy-duty vehicle (RPLP) tax (the energy transport tax is also not paid, as the energy (hydrogen) is produced directly at the production site). Apart from this, the Swiss government has so far refrained from industrial policy measures in the hydrogen sector. The development of the hydrogen economy in Switzerland is currently inhibited by the insufficient production of renewable energy, particularly photovoltaic solar power, as Swiss hydropower currently needs to be used in the first place to meet energy demand in other applications. Changes are needed in the Swiss regulatory framework to boost the development of the hydrogen economy.

The hydrogen revolution accelerates with the current race for a net-zero economy and Switzerland has all the necessary preconditions (energy resources and infrastructure, innovation potential, stable political and macroeconomic situation) to play a leading role in it.

***

* Kateryna Holzer is Senior Researcher at the Centre for Climate, Energy and Environmental Law at the University of Eastern Finland, where she also teaches a course on International Economic Law and Green Transitions. Her research interests in energy law revolve around the role of trade instruments in fostering the transition to a zero-carbon future, including energy taxes, product sustainability standards, and border carbon adjustments.

Download the Paper here ↓

[/av_textblock]

Leave a Reply